Why Cross-Border Payments Still Take Too Long

Payments have never felt faster. Yet settlement has never been the bottleneck it is today. The data explains the gap - and where regulated stablecoins fit.

Cross-border payments have become noticeably easier to initiate. They have not become fundamentally easier to complete. Over the past decade, the industry has invested heavily in improving the customer experience. Payments can now be initiated from a mobile phone, tracked in real time and completed through increasingly intuitive interfaces.

The numbers bear this out. SWIFT reports that around 90% of cross-border payments now reach the destination bank within an hour - comfortably ahead of the G20 and Financial Stability Board target of 75% by 2027. But only about 43% are credited to the end beneficiary's account within that same hour, held up by the final domestic leg of the journey. The instruction is fast; the money often is not.

Yet behind that experience, the underlying infrastructure has changed far less than many assume. Most international payments still rely on correspondent banking networks built around multiple intermediaries, fragmented settlement systems and operating models designed long before today's digital economy.

The result is a contradiction that businesses encounter every day.

Payments appear digital. Settlement remains largely analogue.

As Juha Viitala, Senior Executive Officer at Universal, puts it: “Much of the improvement over the past decade has happened at the edges of the payment journey. The customer experience feels modern, but the payment itself is still handed from one intermediary to the next across systems that were never designed to talk to each other in real time.”

The industry has spent years competing on speed. The next competitive advantage will be infrastructure.The next advantage will be won on infrastructure - and on the settlement layer beneath it.

Speed Is Not the Real Problem

Cross-border payments are often measured by how quickly they are initiated. Businesses measure them differently.

What matters is certainty. When will the funds arrive? What will the transaction ultimately cost? Can the payment be reconciled without manual intervention?

Today's cross-border payment infrastructure struggles to provide those answers consistently because every transaction moves through multiple independent systems.

Correspondent banks apply their own compliance checks, liquidity management processes and operating schedules. Currency conversion introduces additional handoffs. Settlement takes place one institution at a time rather than across a shared infrastructure.

This is why the industry's own targets now reach beyond speed. Alongside the one-hour speed goal, the G20 roadmap sets targets for cost and transparency - a global average retail cost of no more than 1% by 2027, and remittances below 3% by 2030. Certainty, not raw speed, is the benchmark that matters.

Each individual step may seem minor.

Collectively, they create delays, increase costs and reduce transparency across international payments. The challenge is not simply making payments faster. It is reducing the structural friction built into the payment journey itself.

Settlement Is Still the Missing Layer

One of the biggest misconceptions surrounding cross-border payments is that sending money and settling money are the same process. They are not. Payment instructions can move between institutions in seconds.

The money itself only becomes available once every participant in the chain has reconciled balances, updated accounts and reached settlement finality. That distinction explains why businesses can receive confirmation that a payment has been sent while waiting hours, or sometimes days, before those funds can actually be used.

The delay is rarely caused by the message. It is created by the infrastructure responsible for moving value. SWIFT's own data makes the point: the messaging leg has largely met its speed targets, while the gap now sits in the final settlement and last-mile crediting of funds.

The Hidden Cost of Liquidity

Behind every international payment sits another challenge that most businesses never see. Liquidity management.

To support cross-border payments, financial institutions typically maintain pre-funded accounts across multiple countries and currencies so payments can be completed locally. That capital remains tied up while waiting to be used.

The scale is significant, though estimates vary and should be read with care. Banks collectively hold trillions of dollars in pre-funded nostro and vostro balances. A widely cited figure puts gross balances at around $27 trillion - originally a McKinsey estimate, since repeated across the industry - while narrower estimates of the low-yielding capital actually tied up at major correspondents run from several hundred billion to over a trillion. Either way, capital held purely as a settlement buffer is capital not deployed into lending, investment or growth.

Managing liquidity across dozens of payment corridors is operationally complex, particularly as payment volumes shift between markets. It also carries a significant financial cost, especially in lower-volume corridors where capital sits idle for longer periods.

Customers rarely see this machinery. They experience its consequences through higher costs, slower settlement and less predictable payment flows.

Why Better Infrastructure Matters More Than Faster Payments

The conversation around cross-border payments often centres on speed. Speed is an outcome.

Infrastructure is the real differentiator. A payment that arrives in seconds but offers limited transparency, uncertain costs or inconsistent compliance delivers little value to a business operating internationally.

The cost gap is as structural as the speed gap. The World Bank puts the global average cost of sending $200 across borders at 6.36% as of Q3 2025 - and at 14.99% when the sender uses a bank. The UN and G20 target is 3% by 2030. On the same all-in basis, regulated stablecoin rails now settle established corridors for around 1% or less: the on-chain transfer itself costs cents, though fiat on- and off-ramps and FX conversion still apply, so the saving is real but not the near-zero sometimes claimed.

What businesses need is infrastructure that is interoperable, transparent and trusted by design. Financial institutions need payment rails that can exchange both value and data efficiently, operate across jurisdictions and provide greater certainty around settlement.

When the underlying infrastructure improves, speed naturally follows. Focusing on speed alone risks placing faster digital interfaces on top of fragmented financial systems.

Where Digital Assets Can Reduce Friction

Digital assets are often portrayed as a replacement for traditional financial infrastructure. Their greatest opportunity may be something more practical.

Regulated stablecoins can serve as an efficient settlement layer alongside existing banking systems rather than replacing them. Banks, licensed exchanges and payment providers continue to manage customer relationships, compliance and local payment services, while stablecoins help move value more efficiently across the middle of the transaction.

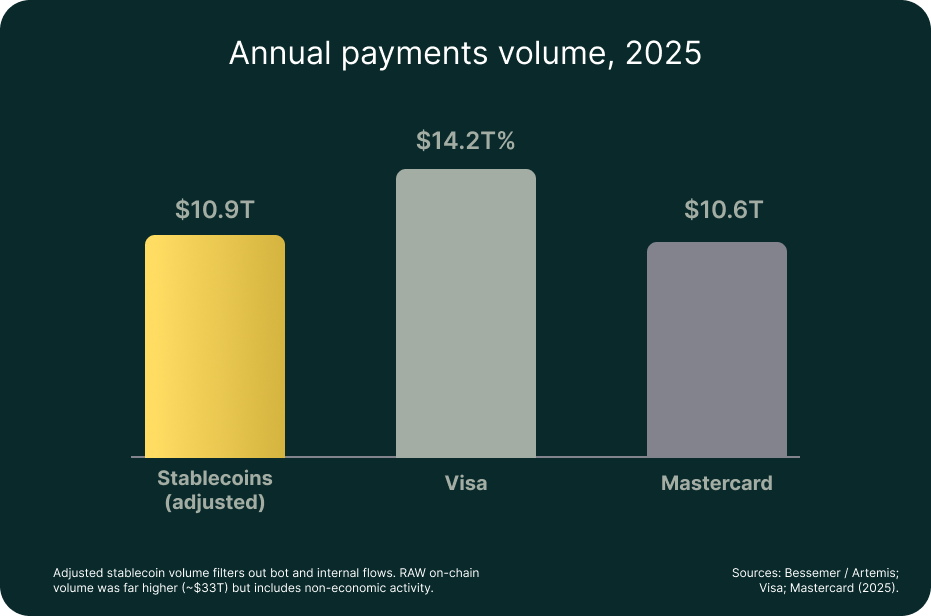

The shift is already measurable - and worth reading carefully. Adjusted stablecoin transaction volume reached roughly $10.9 trillion in 2025, up around 91% year on year and approaching Visa's $14.2 trillion. Headline on-chain figures near $33 trillion overstate genuine activity, because they include automated settlement and internal flows, so the adjusted number is the honest basis for comparison. More telling for institutions: real-world stablecoin payments roughly doubled to about $400 billion in 2025, an estimated 60% of it business-to-business.

The incumbents are validating the direction rather than resisting it. Stripe completed its acquisition of the stablecoin infrastructure firm Bridge for about $1.1 billion in early 2025, and in March 2026 Mastercard agreed to acquire BVNK for up to $1.8 billion — a deal still pending regulatory approval and expected to close by the end of 2026. Two of the largest fintech players are placing billion-dollar bets on the same plumbing within roughly a year.

This approach can shorten settlement times, reduce reliance on pre-funded accounts and improve the movement of liquidity across payment corridors.

The objective is not to replace correspondent banking. It is to remove friction from the parts of the payment journey where today's infrastructure is least efficient.

Why the UAE Is Well Positioned

The UAE occupies one of the world's busiest intersections for trade, remittances and international investment. That creates sustained demand for more efficient cross-border payment infrastructure.

The demand is quantifiable. The UAE is among the world's largest sources of outbound remittances - with cross-border remittance flows estimated at roughly $40 billion or more a year, depending on the source - while domestic payment systems processed more than AED 20 trillion in transfers in the first ten months of 2025 alone.

At the same time, the country has invested in regulatory clarity for digital assets, financial market innovation and next-generation payment infrastructure. That combination matters.

The regulatory groundwork is specific. The Central Bank of the UAE's Payment Token Services Regulation, in force since 2024, requires full reserve backing for payment tokens and reserves everyday domestic payments for dirham-referenced tokens, with foreign payment token is solely for trading of virtual assets and virtual asset derivatives. In practice this suggests a natural division of labour: a dollar-referenced token can carry value efficiently across borders, while the domestic dirham leg settles through regulated dirham-referenced rails. This is the principle underpinning the recently announced AE Coin–USDU collaboration, which enables regulated USD–AED digital settlement within the UAE's evolving financial framework.

Markets rarely become infrastructure leaders through technology alone. They do so by aligning regulation, financial institutions and market infrastructure around practical commercial use cases. The UAE is increasingly demonstrating that approach, positioning itself not only as a hub for digital assets but as a market where the next generation of cross-border payments can be built and tested.

The Future Is Interoperability

The next generation of cross-border payments will not be built on a single rail. It will be built on interoperability.

Instant payment systems, regulated stablecoins, tokenised bank deposits and central bank digital currencies are likely to coexist, connected through common standards that allow value, data and trust to move together more efficiently.

The standards work is already under way. The industry completed its move to the ISO 20022 messaging standard in November 2025, giving payments a common, data-rich language - a precondition for value and information to travel together across otherwise separate systems.

The goal is not to replace one payment system with another. It is to create financial infrastructure that works as seamlessly across borders as information does today.

That is ultimately what businesses have been waiting for.

Not simply faster payments.

Better infrastructure.

About Universal

Universal Digital Intl Limited (“Universal”) is established in the Abu Dhabi Global Market (ADGM) and regulated by the Financial Services Regulatory Authority (FSRA) to conduct the regulated activity of issuing a Fiat-Referenced Token.

Universal is the issuer of USDU, a fully USD-backed stablecoin designed to support secure, transparent, and regulated digital asset settlement. USDU is registered with the Central Bank of the UAE (CBUAE) as a Foreign Payment Token under the Payment Token Services Regulation.

Built on a strong regulatory foundation and supported by trusted institutional partnerships, Universal is advancing resilient digital value infrastructure designed to support the evolving needs of global financial markets.

Learn more at www.universal.ae