Stablecoins 101 for Financial Institutions

A Practical Introduction to Digital Settlement

Stablecoins have become the most institutionally relevant segment of digital assets. For financial institutions, the conversation is no longer about experimentation or market speculation, but about how stablecoins function as regulated settlement infrastructure within existing financial and regulatory frameworks.

This primer is designed for banks, asset managers, payment providers, treasuries, and regulated financial institutions seeking a clear, practical introduction to stablecoins — focusing on structure, regulation, and real-world applicability rather than consumer use cases or market hype.

1. What Is a Stablecoin?

A stablecoin is a digital token designed to maintain a stable value by referencing an underlying asset, most commonly a fiat currency such as the U.S. dollar.

From an institutional perspective, a stablecoin is best understood as a digital representation of fiat value that can be issued, transferred, and settled on blockchain infrastructure.

Unlike volatile cryptocurrencies, properly structured stablecoins are designed to support predictable value transfer, making them suitable for settlement, treasury, and liquidity workflows.

2. Not All Stablecoins Are the Same

Stablecoins differ significantly in design, risk profile, and regulatory treatment. For institutions, these distinctions matter. Key models include:

Fiat-Backed Stablecoins (Fiat-Referenced Tokens)

Stablecoins backed 1:1 by fiat currency reserves held in segregated accounts with regulated financial institutions. When issued under an appropriate regulatory framework, these tokens function as digital settlement instruments rather than speculative assets.

Asset-Backed or Structured Stablecoins

Stablecoins backed by baskets of assets or other financial instruments (including other digital assets). These introduce additional valuation, liquidity, and governance considerations.

Algorithmic Models

Structures that rely on specialized software (algorithms) based on market mechanisms rather than direct reserve backing. These are generally unsuitable for institutional use due to higher structural and stability risk.

For regulated institutions, fully backed, regulated fiat-referenced models are typically the only viable category.

3. Why Institutions Are Adopting Stablecoins

Institutional interest in stablecoins is driven by operational efficiency rather than yield or price appreciation.

Key drivers include:

- Near-real-time settlement compared to legacy multi-day processes

- 24/7 availability, independent of banking cut-off times

- Improved liquidity mobility across entities and markets

- Operational transparency through auditable on-chain records

Stablecoins are increasingly viewed as a new settlement layer, complementing — not replacing — traditional financial infrastructure.

4. Stablecoins as Settlement and Liquidity Infrastructure

For financial institutions, the primary value of stablecoins lies in their role as settlement and liquidity infrastructure — enabling fiat-denominated value to move across company and country borders on blockchain rails with improved speed, predictability, transparency, and operational control.

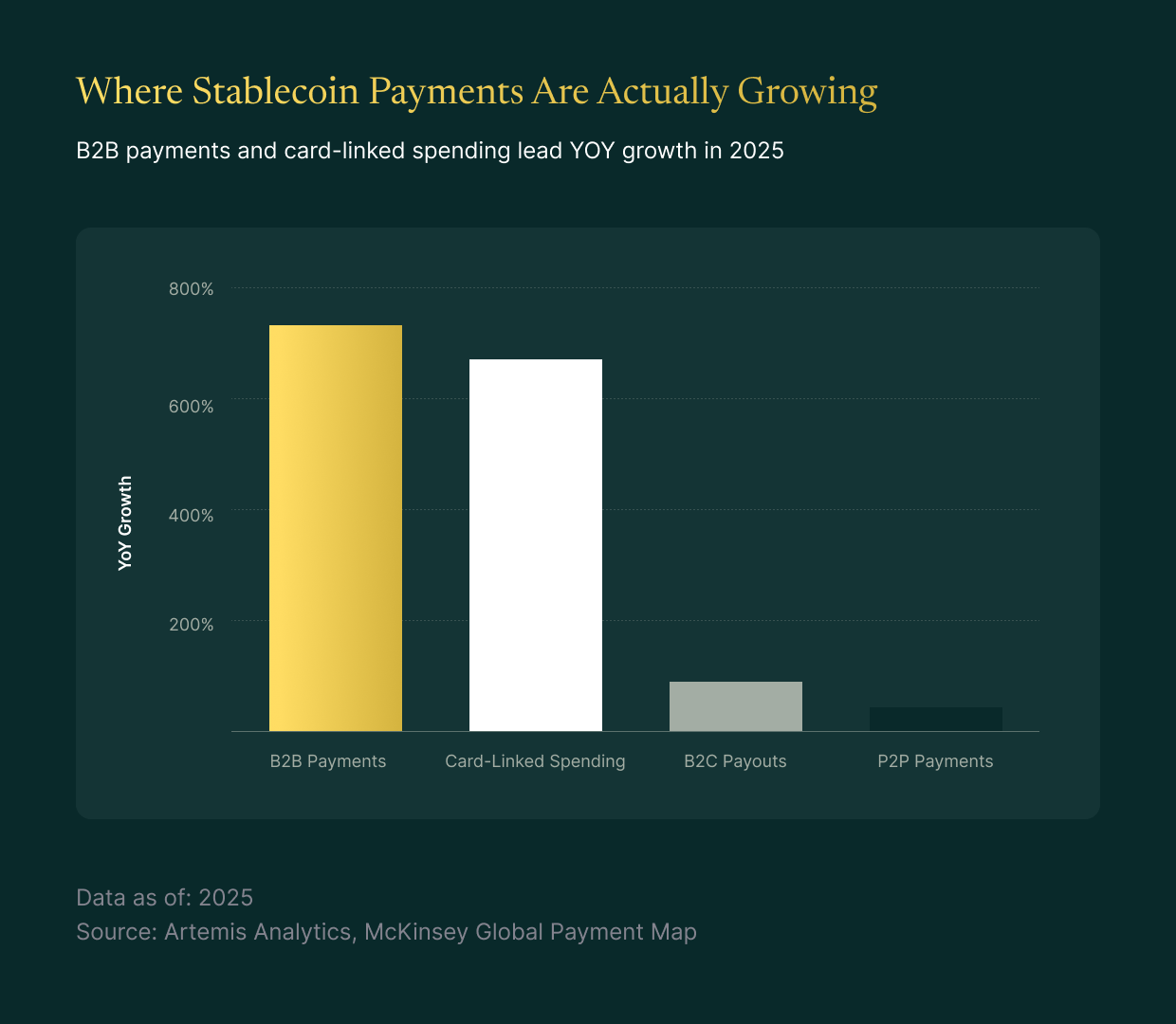

Over the past two years, stablecoins have increasingly shifted from a trading convenience to a high-volume settlement mechanism supporting payments, treasury movements, exchange settlement, and cross-entity liquidity flows.

By late 2025, industry research and on-chain data indicate:

- Annual stablecoin transaction volumes measured in the trillions of U.S. dollars, with estimates ranging between USD 3–5 trillion per year, depending on methodology and inclusion criteria.

- Monthly stablecoin settlement volumes approaching or exceeding USD 800 billion–1 trillion, placing stablecoins among the largest digital payment rails globally by raw value transferred.

- Stablecoins now account for most of all on-chain value transfer, far exceeding the combined transaction volume of non-stablecoin cryptoassets.

Importantly, institutional infrastructure providers report that a growing proportion of this volume is linked to non-speculative activity, including:

- Exchange and market infrastructure settlement

- Treasury and liquidity management between entities

- Cross-border commercial and payment flows

- Collateral movement and margin settlement

This evolution reflects a structural change: stablecoins are increasingly used as operational cash equivalents for digital markets, rather than as instruments held for directional exposure.

Why this matters for institutions

From an institutional lens, stablecoin settlement offers several structural advantages:

- Near-real-time finality, reducing counterparty and settlement risk compared to multi-day legacy processes

- Always-on availability, enabling liquidity movement outside traditional banking hours

- Improved capital efficiency, particularly for entities operating across jurisdictions or legal entities

- High transparency, with auditable transaction records that support reconciliation and oversight

At the same time, stablecoins do not replace banks, payment systems, or existing financial infrastructure. Instead, they function as a new settlement rail that can sit alongside traditional rails — particularly where speed, availability, or cross-border efficiency are critical.

Crucially, institutional suitability depends on governance, reserve structure, redemption certainty, and regulatory oversight — not on the blockchain alone.

5. Regulation: The Defining Constraint

Regulatory clarity is the decisive factor for institutional stablecoin adoption. Across major financial centres, regulators are converging on a common principle: stablecoins used for settlement should be treated as payment-adjacent financial infrastructure — with requirements that resemble prudential standards, market conduct rules, and strong consumer/investor protection where relevant.

What regulators typically supervise

While details vary by jurisdiction, most stablecoin regimes concentrate on five pillars:

- Authorisation and perimeter: who may issue (banks, licensed payment institutions, or specifically authorised stablecoin issuers) and which activities (issuance, custody, brokerage, payments, exchange) fall inside the regulatory scope.

- Reserve quality and safeguarding: what assets may back the token (cash, T‑bills, bank deposits, money market instruments), how they are valued, and whether they must be held with regulated custodians.

- Segregation and bankruptcy remoteness: how client assets are ring-fenced, and what happens in a stress event or issuer insolvency.

- Redemption and operational capability: par redemption, clear timelines/terms, and proven operational processes (including liquidity management under peak demand).

- Governance, disclosures, and assurance: risk management, conflicts controls, disclosures, independent assurance (attestations/audits), and ongoing supervisory reporting.

How major jurisdictions are approaching stablecoins

Regulatory approaches are broadly converging around fiat-referenced stablecoins (sometimes described as e-money tokens, fiat-referenced stablecoins, or payment stablecoins), while imposing stronger restrictions on unbacked or algorithmic models.

A common pattern is emerging:

- License the issuer (and often key service providers such as custodians)

- Set explicit reserve rules (quality, segregation, custody, and independent assurance)

- Standardise redemption obligations (so the token behaves like a reliable settlement unit)

- Define permitted uses (particularly when stablecoins touch domestic payments)

Importantly, stablecoin permissions are often jurisdiction-specific. A token that is suitable for settlement in one market may be restricted or treated differently elsewhere depending on the payment perimeter, licensing category, and how distribution occurs.

In the UAE, for example, stablecoin oversight is structured across coordinated regulatory authorities, separating issuance, market activity, and payment token supervision. This approach provides institutions with defined regulatory perimeters and clearer compliance pathways.

Comparison snapshot: key regulators and regulatory models

What this means for financial institutions

For regulated institutions, the practical implication is a shift from “which stablecoin is popular?” to “which stablecoin is supervised, redeemable, and operationally reliable within our permitted use case?” A simple, institution-friendly diligence lens includes:

- Issuer authorisation: does the issuer have the right license or registration to operate the relevant activity, in the relevant jurisdiction?

- Reserve rules and transparency: are reserves segregated, high-quality, and independently audited and attested?

- Redemption certainty: are there clear, enforceable redemption rights and proven operational capacity?

- Control environment: does the issuer have appropriate governance, risk controls, and reporting?

- Distribution perimeter: are the intended uses and counterparties permitted where you operate?

Note: This is a high-level overview for educational purposes. Requirements differ materially by token type, licensing category, and business model in each jurisdiction.

6. Risk Considerations Institutions Evaluate

While stablecoins reduce certain risks associated with price volatility, they introduce a distinct set of operational, governance, and regulatory considerations that institutions must evaluate with the same rigour applied to any settlement or payment infrastructure.

From an institutional risk perspective, the key question is not whether a stablecoin functions, but whether it can be relied upon under stress, at scale, and within defined regulatory boundaries.

Institutions typically assess the following dimensions:

- Issuer risk

The legal and regulatory status of the issuer, including licensing, supervisory oversight, governance arrangements, financial resilience, and internal control frameworks. Institutions assess whether the issuer is subject to ongoing supervision, clear accountability, and enforceable obligations, particularly in adverse scenarios. - Reserve integrity

The quality, composition, and safeguarding of reserve assets backing the stablecoin. This includes whether reserves are held 1:1, segregated from the issuer’s own assets, custodied with qualified financial institutions, and subject to independent attestation or audit. Reserve structure is central to confidence in par redemption. - Redemption mechanics and liquidity assurance

The issuer’s ability to honour redemptions at par, within defined timeframes, and under periods of elevated demand. Institutions examine redemption terms, operational processes, liquidity management practices, and any gating, throttling, or prioritisation mechanisms that may apply. - Technology and operational risk

Risks arising from smart contracts, blockchain networks, wallet infrastructure, and operational dependencies. This includes network reliability, upgrade governance, incident response procedures, and the maturity of supporting infrastructure such as custody, key management, and transaction monitoring. - Jurisdictional and use‑case constraints

The specific regulatory permissions governing where, how, and by whom the stablecoin may be used. Institutions must ensure that intended uses (such as trading settlement, treasury movements, or payments) are permitted in each relevant jurisdiction and do not inadvertently fall outside regulatory perimeters.

Taken together, these considerations frame stablecoins not as standalone products, but as components of a broader financial control environment.

Regulated issuance models materially mitigate many of these risks by anchoring stablecoins to established supervisory standards, clearly defined permissions, and enforceable governance obligations,aligning stablecoin risk assessment more closely with familiar frameworks used for banks, payment systems, and financial market infrastructure.

Practical mapping: Stablecoin risks and mitigation signals

The table below translates common stablecoin risk categories into practical diligence signals that financial institutions can use when assessing suitability for settlement, treasury, or market infrastructure use.

This mapping reflects how many institutions already assess payment systems, FMIs, and custodians — helping stablecoins fit into existing risk, compliance, and governance frameworks.

7. Integration into Institutional Workflows

Stablecoins can materially improve speed, availability, and operational flexibility, but only when paired with a sufficient level of orchestration: integrating the new settlement rail into existing systems, controls, and responsibilities.

For a traditional financial operator new to digital assets, the new workflow can be understood in two parts :

- A stablecoin that behaves like digital cash on a new rail.

- Integration of the stablecoin into existing workflows; itis less about “crypto” and more about connectivity, controls, reconciliation, and counterparties.

The reality: integration can be the hard part

Even when the token itself is stable, the surrounding operating model needs to be established. Research consistently shows that institutions and corporates view implementation as a systems-and-partnership challenge, not just a product decision.

For example, the EY‑Parthenon Stablecoin Survey (June 2025) found:

- 41% of corporate respondents believe they can integrate stablecoins with moderate effort; 36% say it would require major systems change.

- 63% are looking to traditional banks and financial partners to provide stablecoin capabilities.

- Integration features matter: 56% prioritise embedded APIs into existing treasury/payment platforms, and ~70% would be more willing to adopt stablecoins if integrated into their ERP.

- On the financial institution side, 79% plan to leverage a third party to build out stablecoin infrastructure.

(Source: EY‑Parthenon “Stablecoins in Focus”, June 2025 — link in Source Appendix.)

What “orchestration” typically includes

Stablecoin activity touches multiple functional areas. Common workstreams include:

- On/off ramps and settlement operations: moving between bank money and stablecoins with clear operating procedures

- Wallet and custody controls: secure key management, segregation, approvals, and operational resilience

- Compliance and monitoring: transaction monitoring, sanctions screening, travel rule/recordkeeping expectations (as applicable), audit trails

- Finance operations: reconciliation, statements, accounting treatment, reporting, and internal controls

- Counterparty and vendor management: due diligence and oversight across service providers and venues

Where stablecoins typically sit in the stack

Stablecoins are commonly integrated alongside:

- Custodians and institutional wallet providers, to ensure secure key management and controls comparable to traditional custody

- Trading venues and liquidity providers, where stablecoins act as the settlement asset for market activity and collateral flows

- Treasury and cash management systems, enabling visibility and reconciliation across fiat and on-chain balances

- Compliance, reporting, and audit processes, aligned with existing obligations

The objective is interoperability — stablecoin settlement should operate within established financial operations, governance frameworks, and risk controls.

How institutions get started with stablecoins?

Guiding principle: treat stablecoin integration like onboarding a new settlement rail — phased, governed, and reversible (with backups).

8. Looking Ahead

Stablecoins are moving from “digital assets” into mainstream financial plumbing, with the next phase defined less by token design and more by how stablecoins are embedded into the systems financial operators already use.

What changes in 2026: integration becomes the story

By 2026, the most meaningful progress is expected in distribution and orchestration, including:

- Treasury and ERP integration: stablecoin flows embedded into existing treasury workstations, ERP systems, and cash-management processes (rather than managed in separate “crypto” tools).

- Bank and payment-provider channels: stablecoin capabilities delivered through familiar financial counterparties (accounts, onboarding, reporting), reducing the need for specialist crypto operations.

- Cross-border and market settlement: continued use in exchange settlement, collateral movement, and cross-border B2B value transfer where 24/7 availability and reduced cut-off risk matter most.

- Coexistence with bank-led models: alongside stablecoins, banks are also advancing tokenised deposit and tokenised cash approaches — in many cases targeting similar settlement and cash-management outcomes.

For most institutions, stablecoins will be adopted where they can be made to feel operationally ordinary: controllable, reconcilable, reportable, and integrated.

9. USDU: Institutional USD Settlement, Structured by Design

Within the broader stablecoin landscape, institutional users increasingly differentiate between tokens based on regulatory perimeter, reserve structure, governance standards, and operational design.

USDU is structured specifically for institutional settlement use cases, with a focus on regulatory clarity, conservative reserve management, and controlled issuance.

Core Design Principles

Regulated Issuance

USDU is issued by a regulated entity authorised to conduct the activity of issuing a Fiat‑Referenced Token within Abu Dhabi Global Market (ADGM), under the oversight of the Financial Services Regulatory Authority (FSRA).

Central Bank Registration

USDU is registered as a Foreign Payment Token with the Central Bank of the UAE under the Payment Token Services Regulation (PTSR), defining its permitted use within the UAE’s regulatory perimeter.

Conservative Reserve Structure

USDU is designed to be fully backed 1:1 by USD‑denominated reserves, held with regulated banking partners, prioritising liquidity and high redeemability.

Defined Mint and Redemption Controls

Issuance and redemption are governed by structured processes and oversight mechanisms aligned with regulatory requirements.

Institutional Distribution Infrastructure

USDU is positioned for distribution through regulated institutional channels, supporting compliant onboarding, reporting, and operational integration.

Differentiation in Practice

Compared to offshore or unregulated stablecoin models, USDU’s differentiation rests on:

- Clear regulatory perimeter

- Defined domestic permissions within the UAE

- Institutional governance and oversight

- Structured reserve transparency

- Designed‑for‑settlement positioning rather than retail payment marketing

For institutions operating in or through the UAE — or seeking USD settlement exposure aligned with a regulated financial centre — this structure provides clarity where ambiguity has historically existed in the stablecoin market.

Typical Use Cases

Engage With the Team

Stablecoins are increasingly part of institutional settlement conversations. Whether you are evaluating treasury use cases, market infrastructure integration, or regulated digital settlement within the UAE framework, the next step is structured discussion. To explore how USDU may support your institutional use case within applicable regulatory parameters, connect with the Universal team.

Start the conversation - email info@universal.ae

This content is provided for informational purposes only and is intended for professional audiences. It does not constitute legal, regulatory, or investment advice.

Source Appendix (Selected)

Stablecoin Settlement Volumes & Adoption

- Visa – Onchain Analytics / Crypto Dashboard (2024–2025)

https://www.visa.com/solutions/crypto/onchain-analytics.html - Fireblocks – State of Stablecoins (2024–2025)

https://www.fireblocks.com/reports/state-of-stablecoins/ - Chainalysis – Geography of Cryptocurrency & Stablecoin Briefings (2024–2025)

https://www.chainalysis.com/reports/ - EY‑Parthenon – Stablecoins in Focus (Survey of Corporates & FIs, June 2025)

https://www.ey.com/en_us/insights/financial-services/stablecoins-in-focus - TRM Labs – Crypto & Stablecoin Usage Research (2024–2025)

https://www.trmlabs.com/resources/

Regulatory Frameworks

- EU – Markets in Crypto‑Assets Regulation (MiCA)

https://finance.ec.europa.eu/regulation-and-supervision/financial-services-legislation/markets-crypto-assets_en - UK – HM Treasury / FCA / Bank of England Stablecoin Frameworks

https://www.gov.uk/government/publications/cryptoassets-and-stablecoins - US – Federal Stablecoin Policy & Proposals

https://home.treasury.gov/policy-issues/financial-markets-financial-institutions-and-fiscal-service/digital-assets - Singapore – MAS Stablecoin Regulatory Framework

https://www.mas.gov.sg/regulation/payment-services/stablecoins - Hong Kong – HKMA Stablecoin Regulatory Regime

https://www.hkma.gov.hk/eng/key-functions/international-financial-centre/virtual-assets/ - Japan – JFSA Stablecoin Guidance

https://www.fsa.go.jp/en/policy/digitalassets/ - Switzerland – FINMA Stablecoin Guidance

https://www.finma.ch/en/supervision/fintech/ - UAE – CBUAE Payment Token Services Regulation & ADGM FSRA FRT Framework

https://www.centralbank.ae/en/our-operations/payment-systems/

https://www.adgm.com/operating-in-adgm/financial-services/fintech/crypto-assets

A Practical Introduction to Digital Settlement

Stablecoins have become the most institutionally relevant segment of digital assets. For financial institutions, the conversation is no longer about experimentation or market speculation, but about how stablecoins function as regulated settlement infrastructure within existing financial and regulatory frameworks.

This primer is designed for banks, asset managers, payment providers, treasuries, and regulated financial institutions seeking a clear, practical introduction to stablecoins — focusing on structure, regulation, and real-world applicability rather than consumer use cases or market hype.

1. What Is a Stablecoin?

A stablecoin is a digital token designed to maintain a stable value by referencing an underlying asset, most commonly a fiat currency such as the U.S. dollar.

From an institutional perspective, a stablecoin is best understood as a digital representation of fiat value that can be issued, transferred, and settled on blockchain infrastructure.

Unlike volatile cryptocurrencies, properly structured stablecoins are designed to support predictable value transfer, making them suitable for settlement, treasury, and liquidity workflows.

2. Not All Stablecoins Are the Same

Stablecoins differ significantly in design, risk profile, and regulatory treatment. For institutions, these distinctions matter. Key models include:

Fiat-Backed Stablecoins (Fiat-Referenced Tokens)

Stablecoins backed 1:1 by fiat currency reserves held in segregated accounts with regulated financial institutions. When issued under an appropriate regulatory framework, these tokens function as digital settlement instruments rather than speculative assets.

Asset-Backed or Structured Stablecoins

Stablecoins backed by baskets of assets or other financial instruments (including other digital assets). These introduce additional valuation, liquidity, and governance considerations.

Algorithmic Models

Structures that rely on specialized software (algorithms) based on market mechanisms rather than direct reserve backing. These are generally unsuitable for institutional use due to higher structural and stability risk.

For regulated institutions, fully backed, regulated fiat-referenced models are typically the only viable category.

3. Why Institutions Are Adopting Stablecoins

Institutional interest in stablecoins is driven by operational efficiency rather than yield or price appreciation.

Key drivers include:

- Near-real-time settlement compared to legacy multi-day processes

- 24/7 availability, independent of banking cut-off times

- Improved liquidity mobility across entities and markets

- Operational transparency through auditable on-chain records

Stablecoins are increasingly viewed as a new settlement layer, complementing — not replacing — traditional financial infrastructure.

4. Stablecoins as Settlement and Liquidity Infrastructure

For financial institutions, the primary value of stablecoins lies in their role as settlement and liquidity infrastructure — enabling fiat-denominated value to move across company and country borders on blockchain rails with improved speed, predictability, transparency, and operational control.

Over the past two years, stablecoins have increasingly shifted from a trading convenience to a high-volume settlement mechanism supporting payments, treasury movements, exchange settlement, and cross-entity liquidity flows.

By late 2025, industry research and on-chain data indicate:

- Annual stablecoin transaction volumes measured in the trillions of U.S. dollars, with estimates ranging between USD 3–5 trillion per year, depending on methodology and inclusion criteria.

- Monthly stablecoin settlement volumes approaching or exceeding USD 800 billion–1 trillion, placing stablecoins among the largest digital payment rails globally by raw value transferred.

- Stablecoins now account for most of all on-chain value transfer, far exceeding the combined transaction volume of non-stablecoin cryptoassets.

Importantly, institutional infrastructure providers report that a growing proportion of this volume is linked to non-speculative activity, including:

- Exchange and market infrastructure settlement

- Treasury and liquidity management between entities

- Cross-border commercial and payment flows

- Collateral movement and margin settlement

This evolution reflects a structural change: stablecoins are increasingly used as operational cash equivalents for digital markets, rather than as instruments held for directional exposure.

Why this matters for institutions

From an institutional lens, stablecoin settlement offers several structural advantages:

- Near-real-time finality, reducing counterparty and settlement risk compared to multi-day legacy processes

- Always-on availability, enabling liquidity movement outside traditional banking hours

- Improved capital efficiency, particularly for entities operating across jurisdictions or legal entities

- High transparency, with auditable transaction records that support reconciliation and oversight

At the same time, stablecoins do not replace banks, payment systems, or existing financial infrastructure. Instead, they function as a new settlement rail that can sit alongside traditional rails — particularly where speed, availability, or cross-border efficiency are critical.

Crucially, institutional suitability depends on governance, reserve structure, redemption certainty, and regulatory oversight — not on the blockchain alone.

5. Regulation: The Defining Constraint

Regulatory clarity is the decisive factor for institutional stablecoin adoption. Across major financial centres, regulators are converging on a common principle: stablecoins used for settlement should be treated as payment-adjacent financial infrastructure — with requirements that resemble prudential standards, market conduct rules, and strong consumer/investor protection where relevant.

What regulators typically supervise

While details vary by jurisdiction, most stablecoin regimes concentrate on five pillars:

- Authorisation and perimeter: who may issue (banks, licensed payment institutions, or specifically authorised stablecoin issuers) and which activities (issuance, custody, brokerage, payments, exchange) fall inside the regulatory scope.

- Reserve quality and safeguarding: what assets may back the token (cash, T‑bills, bank deposits, money market instruments), how they are valued, and whether they must be held with regulated custodians.

- Segregation and bankruptcy remoteness: how client assets are ring-fenced, and what happens in a stress event or issuer insolvency.

- Redemption and operational capability: par redemption, clear timelines/terms, and proven operational processes (including liquidity management under peak demand).

- Governance, disclosures, and assurance: risk management, conflicts controls, disclosures, independent assurance (attestations/audits), and ongoing supervisory reporting.

How major jurisdictions are approaching stablecoins

Regulatory approaches are broadly converging around fiat-referenced stablecoins (sometimes described as e-money tokens, fiat-referenced stablecoins, or payment stablecoins), while imposing stronger restrictions on unbacked or algorithmic models.

A common pattern is emerging:

- License the issuer (and often key service providers such as custodians)

- Set explicit reserve rules (quality, segregation, custody, and independent assurance)

- Standardise redemption obligations (so the token behaves like a reliable settlement unit)

- Define permitted uses (particularly when stablecoins touch domestic payments)

Importantly, stablecoin permissions are often jurisdiction-specific. A token that is suitable for settlement in one market may be restricted or treated differently elsewhere depending on the payment perimeter, licensing category, and how distribution occurs.

In the UAE, for example, stablecoin oversight is structured across coordinated regulatory authorities, separating issuance, market activity, and payment token supervision. This approach provides institutions with defined regulatory perimeters and clearer compliance pathways.

Comparison snapshot: key regulators and regulatory models

What this means for financial institutions

For regulated institutions, the practical implication is a shift from “which stablecoin is popular?” to “which stablecoin is supervised, redeemable, and operationally reliable within our permitted use case?” A simple, institution-friendly diligence lens includes:

- Issuer authorisation: does the issuer have the right license or registration to operate the relevant activity, in the relevant jurisdiction?

- Reserve rules and transparency: are reserves segregated, high-quality, and independently audited and attested?

- Redemption certainty: are there clear, enforceable redemption rights and proven operational capacity?

- Control environment: does the issuer have appropriate governance, risk controls, and reporting?

- Distribution perimeter: are the intended uses and counterparties permitted where you operate?

Note: This is a high-level overview for educational purposes. Requirements differ materially by token type, licensing category, and business model in each jurisdiction.

6. Risk Considerations Institutions Evaluate

While stablecoins reduce certain risks associated with price volatility, they introduce a distinct set of operational, governance, and regulatory considerations that institutions must evaluate with the same rigour applied to any settlement or payment infrastructure.

From an institutional risk perspective, the key question is not whether a stablecoin functions, but whether it can be relied upon under stress, at scale, and within defined regulatory boundaries.

Institutions typically assess the following dimensions:

- Issuer risk

The legal and regulatory status of the issuer, including licensing, supervisory oversight, governance arrangements, financial resilience, and internal control frameworks. Institutions assess whether the issuer is subject to ongoing supervision, clear accountability, and enforceable obligations, particularly in adverse scenarios. - Reserve integrity

The quality, composition, and safeguarding of reserve assets backing the stablecoin. This includes whether reserves are held 1:1, segregated from the issuer’s own assets, custodied with qualified financial institutions, and subject to independent attestation or audit. Reserve structure is central to confidence in par redemption. - Redemption mechanics and liquidity assurance

The issuer’s ability to honour redemptions at par, within defined timeframes, and under periods of elevated demand. Institutions examine redemption terms, operational processes, liquidity management practices, and any gating, throttling, or prioritisation mechanisms that may apply. - Technology and operational risk

Risks arising from smart contracts, blockchain networks, wallet infrastructure, and operational dependencies. This includes network reliability, upgrade governance, incident response procedures, and the maturity of supporting infrastructure such as custody, key management, and transaction monitoring. - Jurisdictional and use‑case constraints

The specific regulatory permissions governing where, how, and by whom the stablecoin may be used. Institutions must ensure that intended uses (such as trading settlement, treasury movements, or payments) are permitted in each relevant jurisdiction and do not inadvertently fall outside regulatory perimeters.

Taken together, these considerations frame stablecoins not as standalone products, but as components of a broader financial control environment.

Regulated issuance models materially mitigate many of these risks by anchoring stablecoins to established supervisory standards, clearly defined permissions, and enforceable governance obligations,aligning stablecoin risk assessment more closely with familiar frameworks used for banks, payment systems, and financial market infrastructure.

Practical mapping: Stablecoin risks and mitigation signals

The table below translates common stablecoin risk categories into practical diligence signals that financial institutions can use when assessing suitability for settlement, treasury, or market infrastructure use.

This mapping reflects how many institutions already assess payment systems, FMIs, and custodians — helping stablecoins fit into existing risk, compliance, and governance frameworks.

7. Integration into Institutional Workflows

Stablecoins can materially improve speed, availability, and operational flexibility, but only when paired with a sufficient level of orchestration: integrating the new settlement rail into existing systems, controls, and responsibilities.

For a traditional financial operator new to digital assets, the new workflow can be understood in two parts :

- A stablecoin that behaves like digital cash on a new rail.

- Integration of the stablecoin into existing workflows; itis less about “crypto” and more about connectivity, controls, reconciliation, and counterparties.

The reality: integration can be the hard part

Even when the token itself is stable, the surrounding operating model needs to be established. Research consistently shows that institutions and corporates view implementation as a systems-and-partnership challenge, not just a product decision.

For example, the EY‑Parthenon Stablecoin Survey (June 2025) found:

- 41% of corporate respondents believe they can integrate stablecoins with moderate effort; 36% say it would require major systems change.

- 63% are looking to traditional banks and financial partners to provide stablecoin capabilities.

- Integration features matter: 56% prioritise embedded APIs into existing treasury/payment platforms, and ~70% would be more willing to adopt stablecoins if integrated into their ERP.

- On the financial institution side, 79% plan to leverage a third party to build out stablecoin infrastructure.

(Source: EY‑Parthenon “Stablecoins in Focus”, June 2025 — link in Source Appendix.)

What “orchestration” typically includes

Stablecoin activity touches multiple functional areas. Common workstreams include:

- On/off ramps and settlement operations: moving between bank money and stablecoins with clear operating procedures

- Wallet and custody controls: secure key management, segregation, approvals, and operational resilience

- Compliance and monitoring: transaction monitoring, sanctions screening, travel rule/recordkeeping expectations (as applicable), audit trails

- Finance operations: reconciliation, statements, accounting treatment, reporting, and internal controls

- Counterparty and vendor management: due diligence and oversight across service providers and venues

Where stablecoins typically sit in the stack

Stablecoins are commonly integrated alongside:

- Custodians and institutional wallet providers, to ensure secure key management and controls comparable to traditional custody

- Trading venues and liquidity providers, where stablecoins act as the settlement asset for market activity and collateral flows

- Treasury and cash management systems, enabling visibility and reconciliation across fiat and on-chain balances

- Compliance, reporting, and audit processes, aligned with existing obligations

The objective is interoperability — stablecoin settlement should operate within established financial operations, governance frameworks, and risk controls.

How institutions get started with stablecoins?

Guiding principle: treat stablecoin integration like onboarding a new settlement rail — phased, governed, and reversible (with backups).

8. Looking Ahead

Stablecoins are moving from “digital assets” into mainstream financial plumbing, with the next phase defined less by token design and more by how stablecoins are embedded into the systems financial operators already use.

What changes in 2026: integration becomes the story

By 2026, the most meaningful progress is expected in distribution and orchestration, including:

- Treasury and ERP integration: stablecoin flows embedded into existing treasury workstations, ERP systems, and cash-management processes (rather than managed in separate “crypto” tools).

- Bank and payment-provider channels: stablecoin capabilities delivered through familiar financial counterparties (accounts, onboarding, reporting), reducing the need for specialist crypto operations.

- Cross-border and market settlement: continued use in exchange settlement, collateral movement, and cross-border B2B value transfer where 24/7 availability and reduced cut-off risk matter most.

- Coexistence with bank-led models: alongside stablecoins, banks are also advancing tokenised deposit and tokenised cash approaches — in many cases targeting similar settlement and cash-management outcomes.

For most institutions, stablecoins will be adopted where they can be made to feel operationally ordinary: controllable, reconcilable, reportable, and integrated.

9. USDU: Institutional USD Settlement, Structured by Design

Within the broader stablecoin landscape, institutional users increasingly differentiate between tokens based on regulatory perimeter, reserve structure, governance standards, and operational design.

USDU is structured specifically for institutional settlement use cases, with a focus on regulatory clarity, conservative reserve management, and controlled issuance.

Core Design Principles

Regulated Issuance

USDU is issued by a regulated entity authorised to conduct the activity of issuing a Fiat‑Referenced Token within Abu Dhabi Global Market (ADGM), under the oversight of the Financial Services Regulatory Authority (FSRA).

Central Bank Registration

USDU is registered as a Foreign Payment Token with the Central Bank of the UAE under the Payment Token Services Regulation (PTSR), defining its permitted use within the UAE’s regulatory perimeter.

Conservative Reserve Structure

USDU is designed to be fully backed 1:1 by USD‑denominated reserves, held with regulated banking partners, prioritising liquidity and high redeemability.

Defined Mint and Redemption Controls

Issuance and redemption are governed by structured processes and oversight mechanisms aligned with regulatory requirements.

Institutional Distribution Infrastructure

USDU is positioned for distribution through regulated institutional channels, supporting compliant onboarding, reporting, and operational integration.

Differentiation in Practice

Compared to offshore or unregulated stablecoin models, USDU’s differentiation rests on:

- Clear regulatory perimeter

- Defined domestic permissions within the UAE

- Institutional governance and oversight

- Structured reserve transparency

- Designed‑for‑settlement positioning rather than retail payment marketing

For institutions operating in or through the UAE — or seeking USD settlement exposure aligned with a regulated financial centre — this structure provides clarity where ambiguity has historically existed in the stablecoin market.

Typical Use Cases

Engage With the Team

Stablecoins are increasingly part of institutional settlement conversations. Whether you are evaluating treasury use cases, market infrastructure integration, or regulated digital settlement within the UAE framework, the next step is structured discussion. To explore how USDU may support your institutional use case within applicable regulatory parameters, connect with the Universal team.

Start the conversation - email info@universal.ae

This content is provided for informational purposes only and is intended for professional audiences. It does not constitute legal, regulatory, or investment advice.

Source Appendix (Selected)

Stablecoin Settlement Volumes & Adoption

- Visa – Onchain Analytics / Crypto Dashboard (2024–2025)

https://www.visa.com/solutions/crypto/onchain-analytics.html - Fireblocks – State of Stablecoins (2024–2025)

https://www.fireblocks.com/reports/state-of-stablecoins/ - Chainalysis – Geography of Cryptocurrency & Stablecoin Briefings (2024–2025)

https://www.chainalysis.com/reports/ - EY‑Parthenon – Stablecoins in Focus (Survey of Corporates & FIs, June 2025)

https://www.ey.com/en_us/insights/financial-services/stablecoins-in-focus - TRM Labs – Crypto & Stablecoin Usage Research (2024–2025)

https://www.trmlabs.com/resources/

Regulatory Frameworks

- EU – Markets in Crypto‑Assets Regulation (MiCA)

https://finance.ec.europa.eu/regulation-and-supervision/financial-services-legislation/markets-crypto-assets_en - UK – HM Treasury / FCA / Bank of England Stablecoin Frameworks

https://www.gov.uk/government/publications/cryptoassets-and-stablecoins - US – Federal Stablecoin Policy & Proposals

https://home.treasury.gov/policy-issues/financial-markets-financial-institutions-and-fiscal-service/digital-assets - Singapore – MAS Stablecoin Regulatory Framework

https://www.mas.gov.sg/regulation/payment-services/stablecoins - Hong Kong – HKMA Stablecoin Regulatory Regime

https://www.hkma.gov.hk/eng/key-functions/international-financial-centre/virtual-assets/ - Japan – JFSA Stablecoin Guidance

https://www.fsa.go.jp/en/policy/digitalassets/ - Switzerland – FINMA Stablecoin Guidance

https://www.finma.ch/en/supervision/fintech/ - UAE – CBUAE Payment Token Services Regulation & ADGM FSRA FRT Framework

https://www.centralbank.ae/en/our-operations/payment-systems/

https://www.adgm.com/operating-in-adgm/financial-services/fintech/crypto-assets