From Correspondent banking to Tokenised Settlement

Why Financial Institutions Are Rethinking How Value Moves

For decades, international finance has relied on correspondent banking networks and nostro accounts to move money across borders.

The system works, but it was designed for a world where markets operated within fixed hours and settlement timelines were measured in days.

Today’s financial markets look very different.

Digital asset markets operate 24 hours a day, global trading venues are interconnected, and capital moves continuously across jurisdictions.

Yet the infrastructure used to settle transactions often still relies on multi-day settlement cycles and prefunded liquidity accounts.

For financial institutions and treasury teams, this creates a structural inefficiency: markets have become real-time, while settlement has not.

The Cost of the Legacy Model

To facilitate international payments, banks maintain nostro accounts with correspondent institutions across multiple currencies and jurisdictions.

These accounts must be prefunded to ensure transactions can settle reliably.

Industry estimates suggest that $3–5 trillion of liquidity globally sits idle in nostro accounts, effectively locked within the settlement infrastructure itself.

This model also introduces operational complexity:

- multiple intermediaries

- reconciliation across institutions

- settlement delays across time zones

For institutions operating in global markets, liquidity must often be distributed rather than dynamically deployed.

Tokenised Settlement: A Different Model

Stablecoins introduce an alternative settlement architecture.

Rather than relying on correspondent banking chains, stablecoins represent tokenised claims on fiat reserves, enabling value to move directly across blockchain networks.

This changes the mechanics of settlement.

Traditional Settlement

Tokenised Settlement

Multiple intermediaries

Direct transfer

T+1 to T+3 settlement

Near-instant settlement

Banking hours

24/7 availability

Prefunded liquidity

On-chain liquidity

For financial institutions operating in continuous markets, faster settlement can translate into greater capital efficiency and improved liquidity mobility.

A Rapidly Growing Settlement Layer

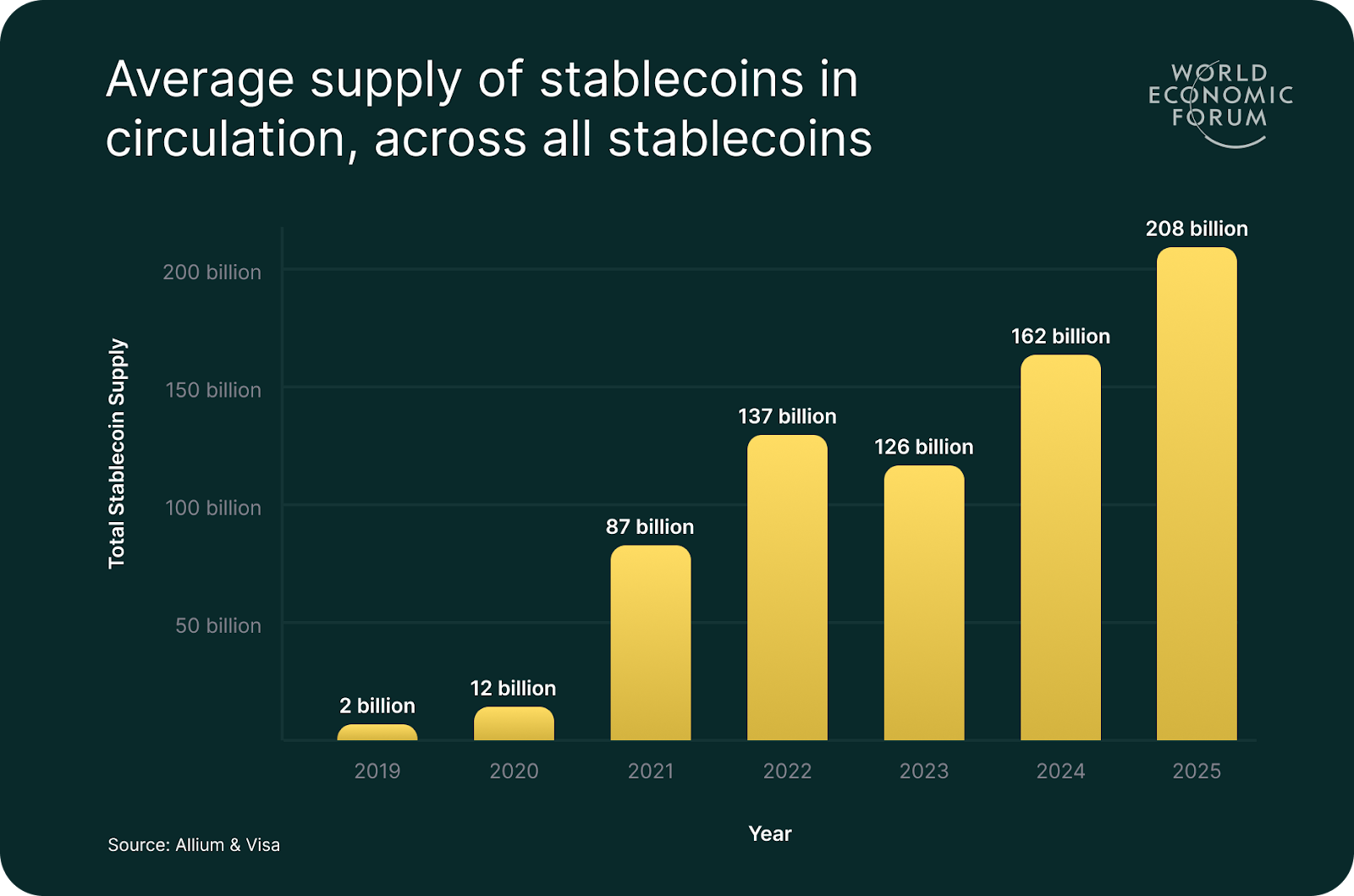

Stablecoins have evolved quickly from niche instruments into a major component of digital financial infrastructure.

Circulating supply has grown from approximately $2 billion in 2019 to nearly $280 billion by 2025.

Transaction activity has grown even faster.

Stablecoin networks now process more than $15 trillion in annual transaction volume, driven largely by trading settlement, liquidity management, and on-chain financial activity.

Where Institutions Are Using Stablecoins Today

Stablecoins are increasingly used in several operational contexts:

Exchange settlement

Digital asset trading venues use stablecoins as the primary settlement asset for many trading pairs.

Collateral and margin management

Institutions can post margin and rebalance collateral between venues in near real time.

Treasury liquidity mobility

Stablecoins allow capital to move across entities and markets without relying on correspondent banking flows.

In these contexts, stablecoins function less as a speculative asset and more as settlement infrastructure for digital markets.

Institutional Trust and Regulation

For financial institutions, adoption ultimately depends on governance and regulatory oversight.

Stablecoins designed for institutional use typically incorporate:

- fully backed fiat reserves

- segregated reserve accounts

- independent reserve attestations

- regulated issuers

For example, USDU is issued by Universal Digital Intl Limited, regulated by the Financial Services Regulatory Authority in Abu Dhabi Global Market and registered with the Central Bank of the UAE as a Foreign Payment Token, with reserves fully backed by U.S. dollars held with UAE banking partners.

.png)

A New Layer of Financial Infrastructure

Stablecoins are unlikely to replace the banking system.

Banks remain essential for custody, compliance, and access to fiat liquidity.

However, tokenised settlement introduces a new infrastructure layer that can complement traditional payment systems.

For institutions operating in global digital markets, the shift is already underway.

The underlying driver is simple:

capital now moves faster than the infrastructure originally designed to settle it.

Resource Index

- Bank for International Settlements – The Future Monetary System

https://www.bis.org/publ/arpdf/ar2022e3.htm - McKinsey – Global Payments Report

https://www.mckinsey.com/industries/financial-services/our-insights/global-payments-report - Citi GPS – Money, Tokens, and Games

https://www.citigroup.com/global/insights/money-tokens-and-games - Chainalysis – Stablecoin Adoption & Market Reports

https://www.chainalysis.com/reports - European Union – Markets in Crypto-Assets Regulation (MiCA)

https://finance.ec.europa.eu/digital-finance/markets-crypto-assets-regulation-mica_en

About Universal

Universal Digital Intl Limited (“Universal”) is established in the Abu Dhabi Global Market (ADGM) and regulated by the Financial Services Regulatory Authority (FSRA) to conduct the regulated activity of issuing a Fiat-Referenced Token.

Universal is the issuer of USDU, a fully USD-backed stablecoin designed to support secure, transparent, and regulated digital asset settlement. USDU is registered with the Central Bank of the UAE (CBUAE) as a Foreign Payment Token under the Payment Token Services Regulation.

Built on a strong regulatory foundation and supported by trusted institutional partnerships, Universal is advancing resilient digital value infrastructure designed to support the evolving needs of global financial markets.

Learn more at www.universal.ae